I want to start by saying that I am not a doctor. I am not a nurse or a scientist...

Read More

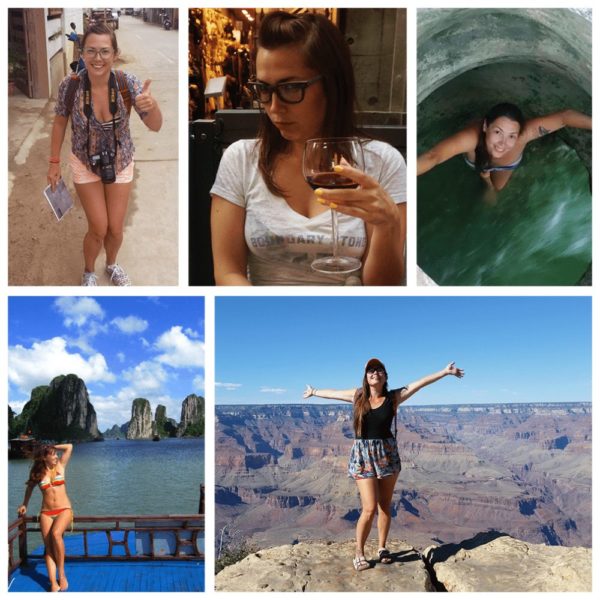

Have you ever wanted to run away from your boring job and take all the chances you thought you missed? Well I did. After five years working in finance I dropped it all to make sure my life was really worth living. And I never looked back. From being unemployed, to working in bars, to teaching English and now full-time freelancing, I’m making my way around the world.

I have one rule in life: do whatever you want. Don’t let anyone tell you any different. It’s all too easy to get caught up making choices because you think you’re supposed to, or to please other people, or to follow in your parents’ footsteps. Once you realize that what you want doesn’t have to align with anyone else’s ideas of who you are, the whole world will open up for you.

Wanna see how easy it is? Follow my peripatetic adventures and careless calamities as I chase down adventure and the thrill of the unknown from corner to corner of this crazy planet.

Have you ever been walking through a neighborhood in a foreign city when the feeling you definitely should not be…

Just after we moved to Cape Town, my husband and I realized that our American Airlines miles didn’t do a…